TDS UNDER GST (Section 51 of CGST Act, 2017)

TDS Under GST (Section 51 of CGST Act, 2017): Complete Guide

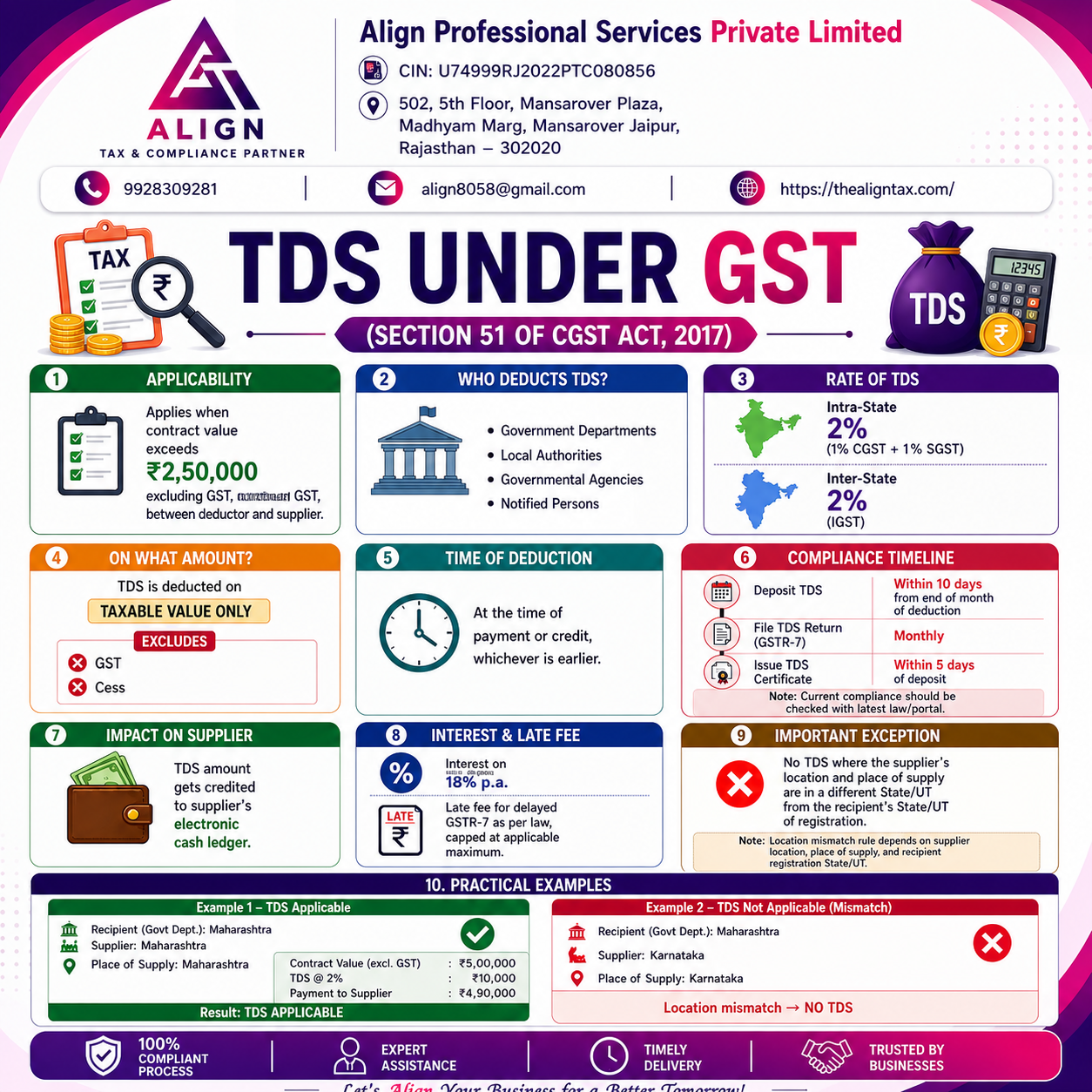

In GST compliance, Tax Deducted at Source (TDS) plays a crucial role in ensuring transparency and timely tax collection. Section 51 of the CGST Act governs TDS provisions under GST.

This article explains applicability, rates, compliance, and practical scenarios in a simple and professional manner.

1. Applicability of TDS Under GST

TDS under GST is applicable when:

- The contract value exceeds ₹2,50,000 (excluding GST)

- The transaction is between a deductor and supplier

👉 Note: GST amount is not included while calculating the threshold.

2. Who is Required to Deduct TDS?

The following entities are required to deduct TDS:

- Government Departments

- Local Authorities

- Governmental Agencies

- Notified Persons (as per GST law)

3. Rate of TDS

TDS is deducted at a rate of 2%, depending on the nature of supply:

- Intra-State Supply:

1% CGST + 1% SGST - Inter-State Supply:

2% IGST

4. On What Amount is TDS Deducted?

TDS is deducted on:

✔ Taxable Value only

Exclusions:

- GST

- Cess

👉 This means TDS is not calculated on the total invoice value including tax.

5. Time of Deduction

TDS must be deducted at the earlier of:

- Time of payment, or

- Time of credit to supplier

6. Compliance Timeline

To ensure proper compliance, the following timelines must be followed:

- Deposit of TDS:

Within 10 days from the end of the month of deduction - Return Filing (GSTR-7):

Monthly basis - TDS Certificate (GSTR-7A):

Within 5 days of deposit

👉 Always verify updates from the GST portal for latest changes.

7. Impact on Supplier

The deducted TDS amount is credited to the supplier’s:

➡ Electronic Cash Ledger

This amount can be used by the supplier to pay GST liabilities.

8. Interest and Late Fee

Non-compliance attracts penalties:

- Interest on Late Payment: 18% per annum

- Late Fee for GSTR-7 Delay:

Applicable as per GST law (subject to maximum cap)

9. Important Exception (Location Mismatch Rule)

TDS is not applicable when:

- Supplier’s location and place of supply are in a different State/UT, AND

- Recipient is registered in another State/UT

👉 In such cases, location mismatch = No TDS

10. Practical Examples

✅ Example 1: TDS Applicable

- Recipient: Maharashtra (Govt Dept.)

- Supplier: Maharashtra

- Place of Supply: Maharashtra

- Contract Value (Excl. GST): ₹5,00,000

- TDS @ 2%: ₹10,000

- Net Payment: ₹4,90,000

👉 Conclusion: TDS Applicable

❌ Example 2: TDS Not Applicable

- Recipient: Maharashtra

- Supplier: Karnataka

- Place of Supply: Karnataka

👉 Conclusion: Location mismatch → No TDS

Conclusion

TDS under GST is a compliance-driven mechanism aimed at improving tax collection efficiency. Understanding its applicability, rates, and timelines is essential for avoiding penalties and ensuring smooth compliance.

Businesses and government entities must regularly review their transactions and maintain proper documentation to stay compliant.

Need Expert Assistance?

At Align Professional Services Pvt. Ltd., we help businesses with:

Have Questions? We're Here to Help

Get expert advice from Align Professional Services Private Limited. Reach out to discuss your requirements.