Form 121 (UIN) – New TDS Declaration Rule from April 2026

Form 121 (UIN) – New TDS Declaration System from April 2026

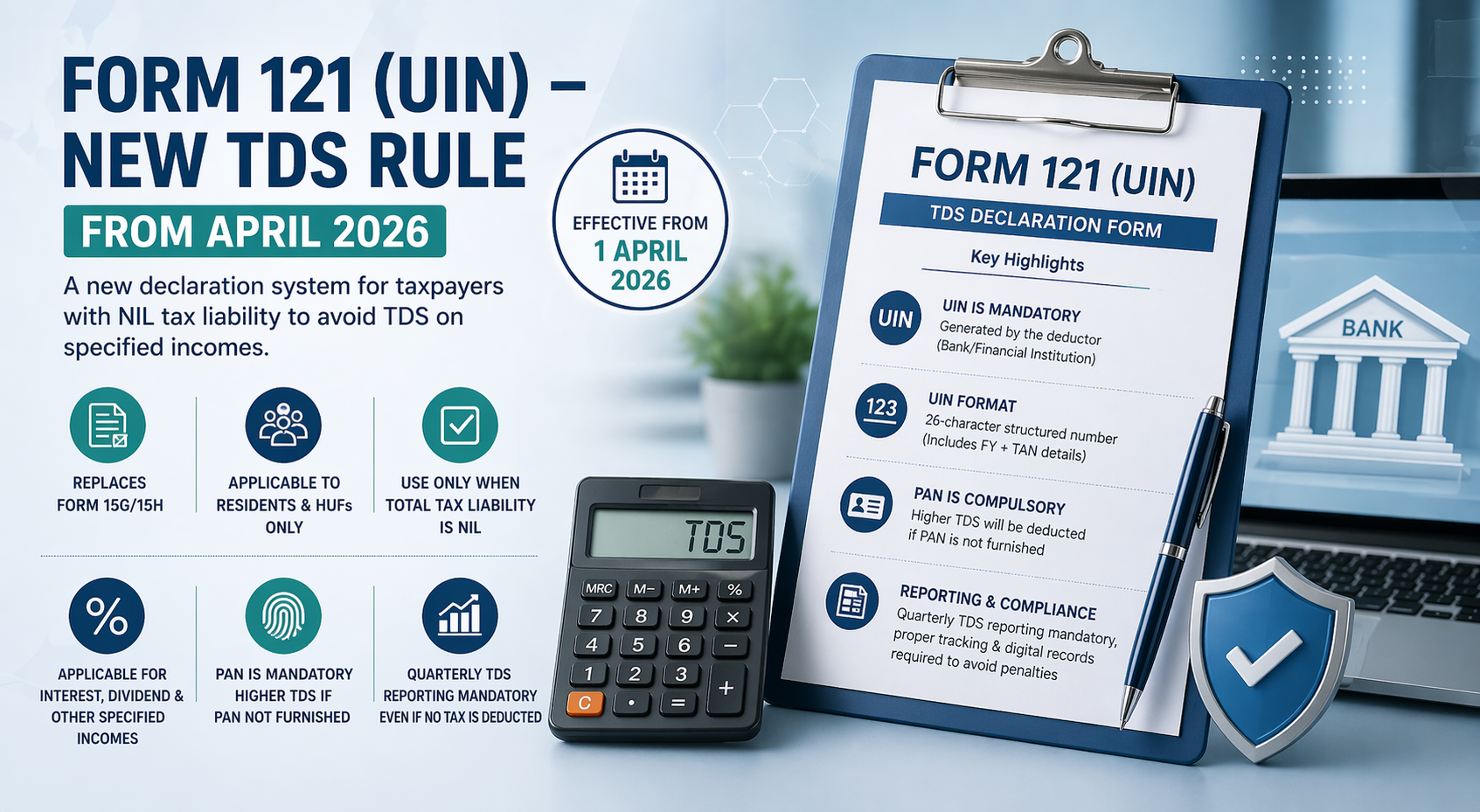

The Income-tax Department has introduced Form 121 with a Unique Identification Number (UIN) as a replacement for Forms 15G and 15H. This reform aims to enhance transparency, traceability, and compliance in TDS declarations.

📌 What is Form 121?

Form 121 is a self-declaration form that allows eligible taxpayers to declare that their total tax liability for the financial year is NIL, thereby requesting the deductor not to deduct TDS on specified incomes.

This concept continues under the framework of Section 197A of the Income-tax Act, 1961, which governs non-deduction of TDS based on declarations.

📅 Effective Date

- Applicable from 1st April 2026

- Forms 15G and 15H will be discontinued from this date

👤 Eligibility Criteria

Form 121 can be filed by:

- ✔️ Resident Individuals

- ✔️ Hindu Undivided Families (HUFs)

Not applicable to:

- ❌ Non-Residents (NRIs)

- ❌ Firms, LLPs, Companies, or other entities

⚖️ Key Condition for Submission

- The taxpayer’s total estimated income must result in NIL tax liability

If this condition is not satisfied:

- ❌ Form 121 cannot be submitted

- ✔️ TDS will be deducted at applicable rates

💰 Types of Income Covered

Form 121 is generally applicable to incomes such as:

- Interest Income (Fixed Deposits, Recurring Deposits, Savings Accounts)

- Dividend Income

- Other specified incomes covered under TDS provisions

🔢 UIN (Unique Identification Number) – Mandatory Feature

A key enhancement in the new system is the introduction of UIN-based tracking:

- Each Form 121 must have a mandatory UIN

- UIN will be generated by the deductor (e.g., banks or financial institutions)

- Enables:

- Accurate tracking of declarations

- Prevention of duplication or misuse

- Improved audit and verification

🧾 UIN Structure

- A 26-character alphanumeric code

- Typically includes:

- Financial Year

- TAN of the deductor

- Serial sequence

This ensures end-to-end traceability in the TDS system.

🆔 PAN Requirement

- PAN is mandatory while submitting Form 121

If PAN is not provided:

- ❌ TDS will be deducted at higher rates as per Income-tax provisions

📊 Reporting & Compliance Requirements

Deductors must ensure:

- 📌 Quarterly TDS returns must be filed, even if no tax is deducted

- 📌 Proper UIN-wise reporting and reconciliation

- 📌 Maintenance of digital records and audit trail

Non-compliance may lead to:

- Penalties under TDS provisions

- Increased scrutiny from the Income-tax Department

🚨 Practical Impact

For Taxpayers:

- Simplified but more controlled declaration process

- Need for accurate income estimation

- Reduced scope for misuse

For Deductors:

- Additional responsibility of UIN generation and tracking

- System upgrades for compliance and reporting

- Mandatory reporting even in NIL TDS cases

📝 Conclusion

The introduction of Form 121 with UIN marks a significant step towards digitization and better compliance in the TDS ecosystem. While it strengthens monitoring and reduces misuse, both taxpayers and deductors must ensure accurate, timely, and compliant filings.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from Align Professional Services Private Limited. Reach out to discuss your requirements.